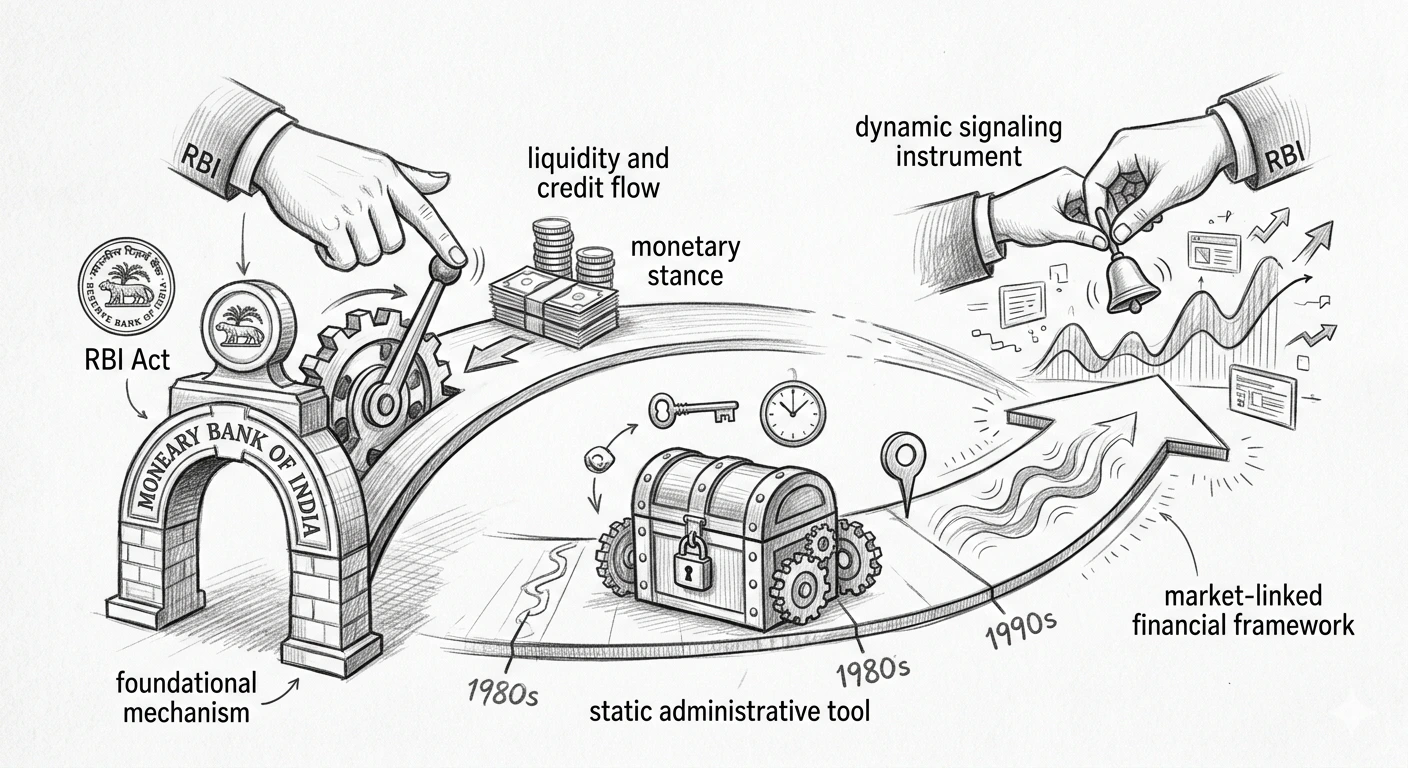

The Bank Rate Policy in India serves as the foundational mechanism for monetary regulation, acting as the primary lever through which the Reserve Bank of India (RBI) manages liquidity and credit flow. Established as a critical component of the RBI Act, this rate dictates the cost of long-term borrowing and rediscounting for commercial entities, signifying the central bank’s monetary stance. Its evolution from a static administrative tool in the 1980s to a dynamic signaling instrument in the 1990s highlights India's transition toward a market-linked financial framework, ensuring stability during periods of economic volatility and liberalization.

The Narrative of Monetary Control: Defining the Bank Rate

The operational framework of the Indian financial market relies heavily on structured regulatory benchmarks to balance systemic credit expansion. Within this environment, the central banking apparatus employs long-term discount windows to communicate its policy goals to scheduled commercial operations across the nation.

- Defining the Core Regulatory Instrument

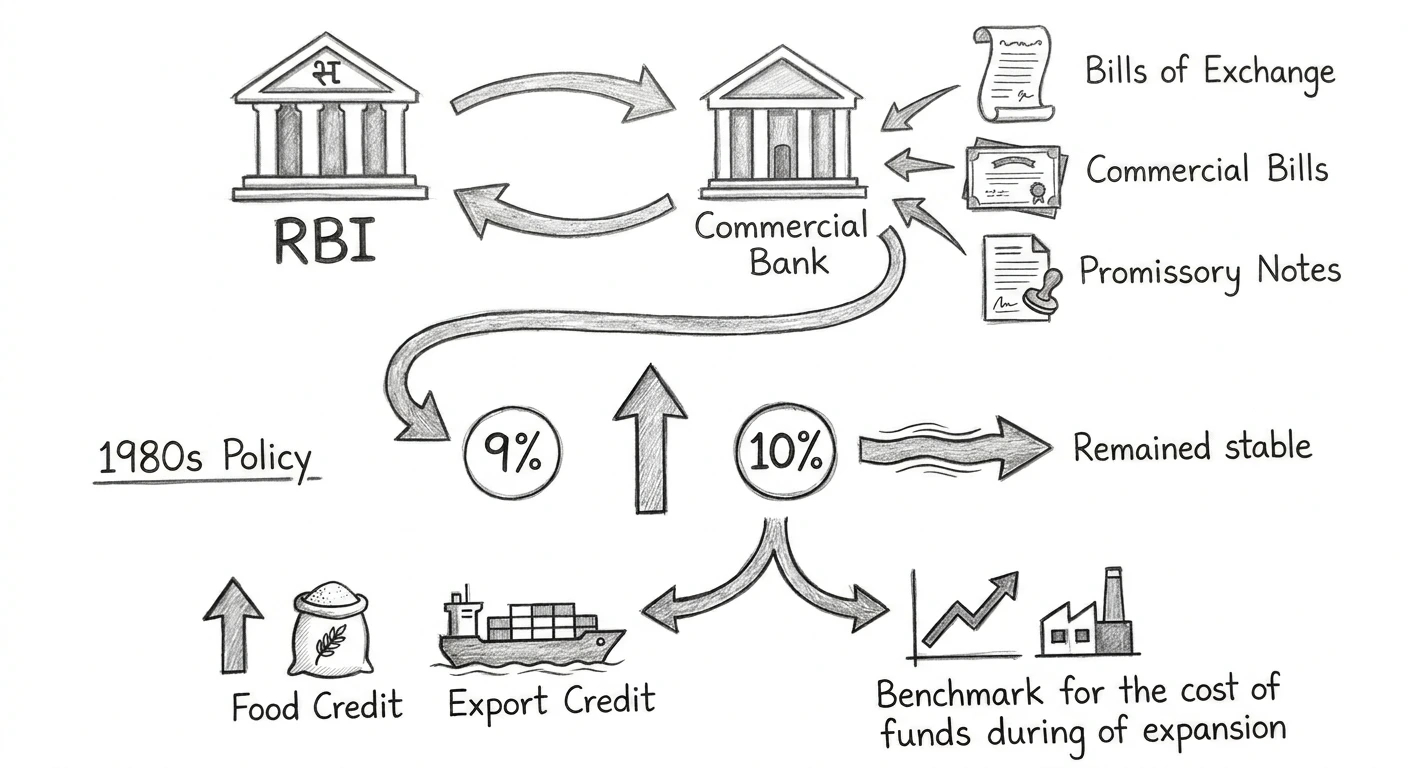

In the technical landscape of Indian finance, the bank rate is legally anchored by the RBI Act. Bank Rate is the interest rate at which the Reserve Bank of India (RBI) lends money to commercial banks or helps them get cash by buying certain financial documents like:

- Bills of Exchange – Written promises that one party will pay another party a specific amount on a future date.

- Commercial Bills – Short-term credit documents used in trade and business transactions.

- Promissory Notes – Written promises to pay a certain amount at a specified time.

- Other RBI-approved short-term debt instruments used by banks and businesses.

This definition establishes the RBI as the lender of last resort, providing a corridor for banking operations. The Chakravarty Committee report further solidified its significance, noting that the RBI could effectively steer banking behavior and national credit trends through proactive adjustments of this policy rate.

Analyzing the Bank Rate Policy During the 1980s

The domestic monetary framework during the pre-liberalization era prioritized direct administrative management over variable market indicators. Policy mechanisms were intentionally insulated to provide prolonged structural predictability across public sector financing corridors.

The Era of Regulatory Stability and Committee Insights

During the 1980s, the Indian economy operated under a regime of tightly controlled interest rates, where the bank rate acted as a stable anchor for the broader financial system. Significant movement occurred in July 1981, when the bank rate was increased from 9% to 10%. This adjustment was not an isolated event; it triggered a corresponding rise in refinance rates specifically for food and export credit, impacting various special lending facilities. Despite the Chakravarty Committee's emphasis on its power, the policy landscape remained remarkably consistent for the remainder of the decade. Consequently, the bank rate remained fixed at 10% throughout the late 1980s, lasting until the economic shifts of 1991-92.

- (i) Interest rates on RBI credit to the commercial sector were directly linked to the bank rate.

- (ii) The rate served as a benchmark for the cost of funds during a period of industrial expansion.

The Great Reactivation: Developments in the 1990s Reform Era

The opening up of the domestic market demanded a fundamental realignment of traditional central banking levers. As rigid administrative dictates gave way to competitive treasury operations, older transmission paths were overhauled to match fluid capital flows.

Strategic Repositioning as a Monetary Signaling Tool

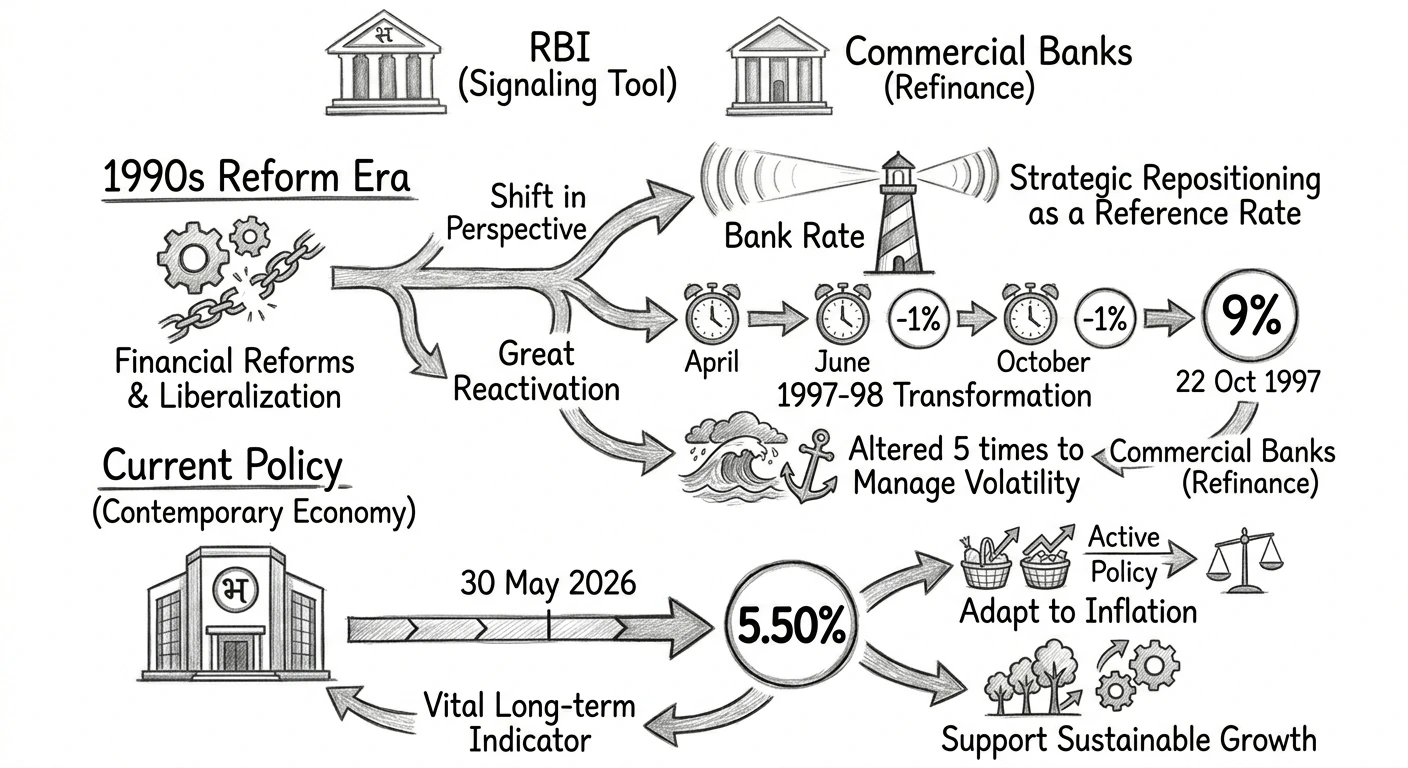

The dawn of financial sector reforms in the early 1990s initially saw the bank rate take a backseat as newer instruments emerged. However, this dormancy was short-lived as the liberalization era required more sophisticated market signals. By the mid-1990s, the RBI reactivated the bank rate, transforming it into a reference rate for the entire financial system. During the fiscal year of 1997-98, the rate underwent a radical transformation, being repositioned to reflect real-time liquidity conditions. To mirror an easing liquidity environment, the RBI executed three successive 1% reductions during April, June, and October 1997. By October 22, 1997, the rate was successfully calibrated down to 9% per annum.

- (i) The bank rate was altered five times during 1997–98 to manage post-liberalization volatility.

- (ii) It serves as the benchmark rate at which refinance is granted to commercial banks.

Summary: Current Standing and Modern Economic Relevance

Modern credit coordination relies on a mix of high-frequency liquidity operations and long-term stabilization benchmarks. While short-term adjustments dominate daily operations, the primary window anchors the ultimate cost of institutional defaults and structural facilities.

- Contemporary Economic Alignment

In the contemporary economic landscape, the Bank Rate Policy remains a vital indicator of the RBI's long-term monetary perspective. As of 2026, the current bank rate in India stands at 5.50%. This modern valuation highlights the ongoing evolution of the rate from a rigid 1980s administrative figure to an active, flexible instrument within a globalized economy. By functioning as both a signalling tool and a regulatory benchmark, the bank rate ensures that the Indian financial system can adapt to inflationary pressures while supporting sustainable growth trajectories.

Quick Revision Points for Students

Reviewing the historical development and legal provisions guarantees retention for competitive examinations:

- (i) The rate is statutorily governed under the provisions of the RBI Act for rediscounting commercial paper.

- (ii) It reached an administrative consolidation high of 10% in July 1981, staying locked there for a decade.

- (iii) The instrument was reactivated as a flexible reference rate during the structural adjustments of 1997–98.

- (iv) It serves as the baseline yardstick for computing penal interest rates on commercial banks failing reserve goals.

Frequently Asked Questions (FAQ)

Q1: How does the Bank Rate differ from short-term liquidity tools like Repo Rate?

A1: The Bank Rate deals primarily with long-term institutional borrowing and asset rediscounting without collateral requirements under the RBI Act, whereas the Repo Rate handles short-term liquidity backstops secured by government backing instruments.Q2: What major shift did the bank rate undergo during the fiscal phase of 1997-98?

A2: The rate transitioned from a dormant administrative anchor to an active market signaling tool, undergoing five separate revisions within a single fiscal year, including three consecutive drops to hit 9% in October 1997.Q3: What role does the Bank Rate play in penalizing commercial banking entities today?

A3: It serves as the institutional benchmark for penal charges. If scheduled banks fall short of their mandated cash reserve ratio (CRR) or statutory liquidity ratio (SLR) limits, fines are levied at fixed percentage marks above the operational bank rate.