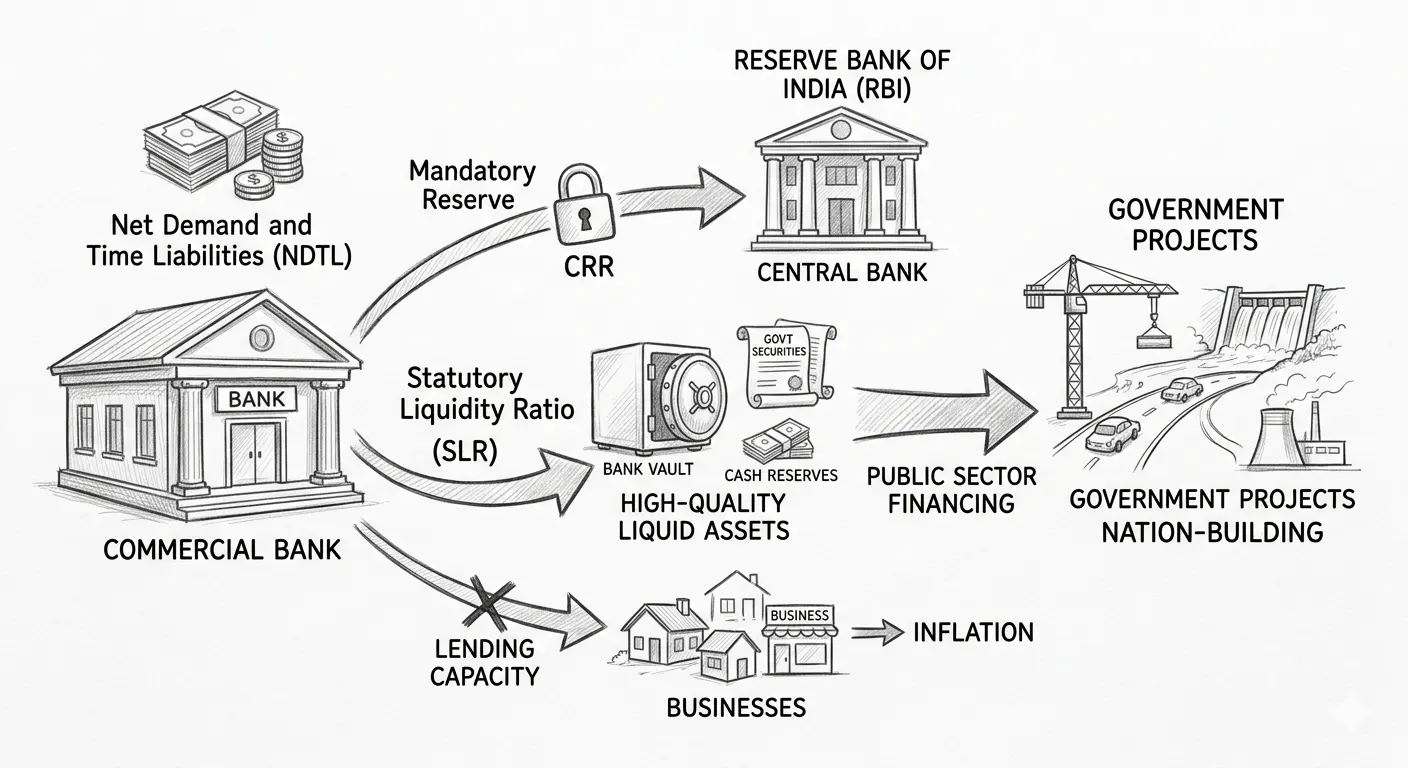

The Statutory Liquidity Ratio (SLR) stands as a cornerstone of Indian monetary policy, functioning as a vital instrument used by the Reserve Bank of India (RBI) to ensure financial discipline. Historically, its significance peaked during the late 20th century, serving as a dual-purpose tool: it managed inflationary pressures by restricting the lending capacity of commercial banks while simultaneously securing a guaranteed market for government securities. By mandating that banks maintain a specific portion of their Net Demand and Time Liabilities (NDTL) in safe, liquid forms, the SLR framework provided the institutional stability necessary for the nation's fiscal expansion and public sector financing during critical developmental decades.

The Narrative of Financial Stability: Defining SLR in India

- The Structural Logic of Central Banking Prudentials

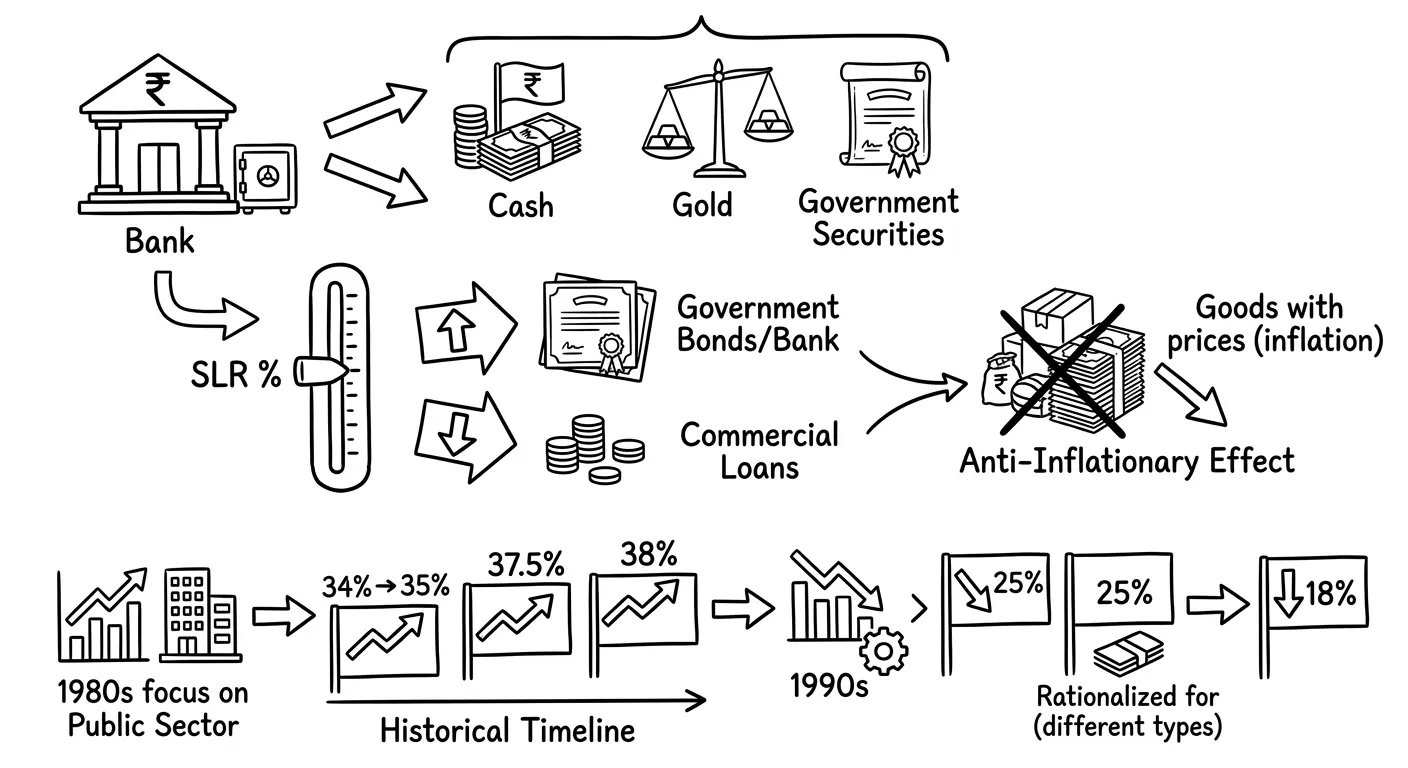

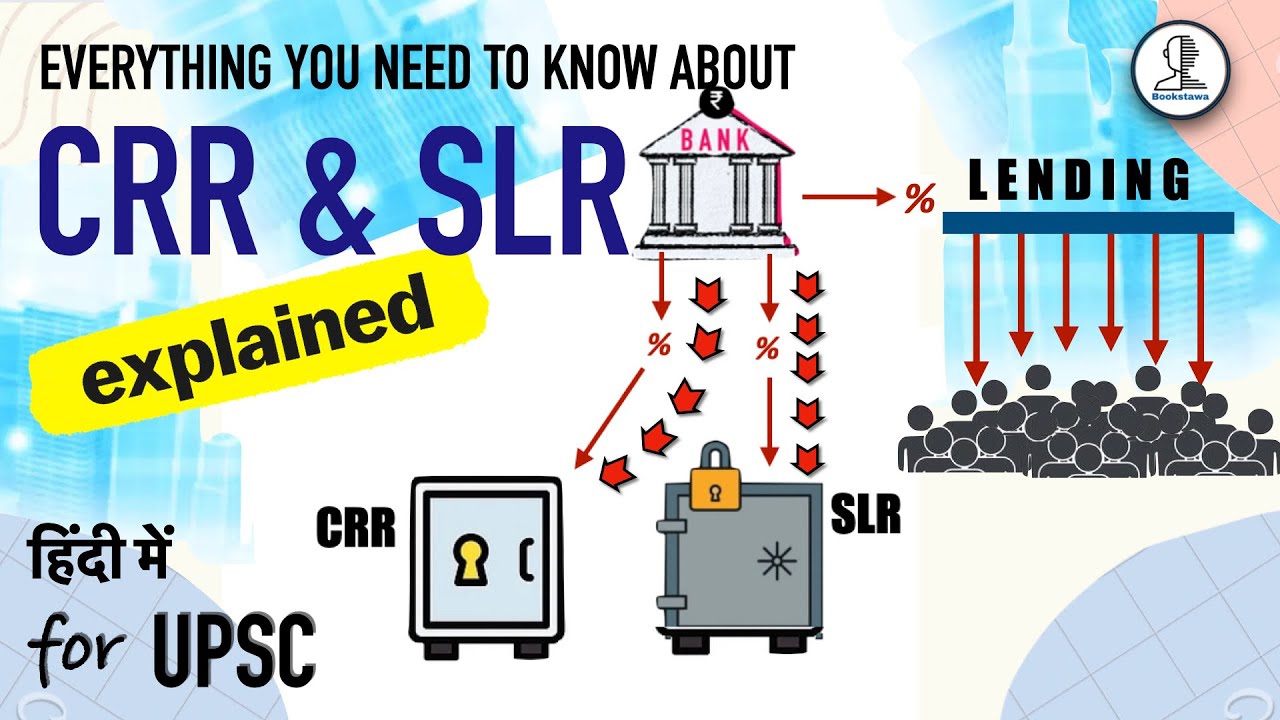

In the complex landscape of Indian Central Banking, the SLR acts as a mandatory buffer. Unlike the Cash Reserve Ratio (CRR), which deals strictly with cash kept with the RBI, the Statutory Liquidity Ratio requires banks to maintain a reserve of high-quality liquid assets within their own vaults. This narrative of prudence and liquidity ensures that even in times of economic stress, banks possess the solvency to meet depositor demands while funneling capital into nation-building projects through approved securities.

Analyze the Definition and Core Functions of SLR

The technical ratio between liquid assets and the demand and time liabilities held by Indian banks is formally defined as the Statutory Liquidity Ratio. It serves as a regulatory valve for the entire economy.

Explore the Mechanics of Liquid Assets and Bank Liabilities

Under the statutory mandate, banks must divert a portion of their resources away from commercial lending. This categorization of liquid assets includes gold, physical cash, and government-approved securities. When the RBI enforces a higher SLR, it intentionally reduces the loanable funds available to the private sector, creating a powerful anti-inflationary effect. Furthermore, this mechanism influences public sector financing by directing bank capital toward state-backed debt instruments.

- (i) Liquid assets provide an immediate safety net for bank depositors.

- (ii) Mandatory investments in securities ensure fiscal stability for the government.

Deep Dive into SLR Policy Adjustments During the 1980s and 1990s

The 1980s represented a period of active liquidity regulation. The RBI utilized the SLR extensively to support public sector investment goals without the inflationary risk of printing new reserve money.

Chronicle of Historical Rate Changes and Statutory Mandates

The timeline of SLR adjustments reflects the shifting priorities of the Indian economy. In October 1981, the rate was moved from 34% to 35% across two distinct phases. By April 25, 1987, the requirement was hiked to 37.5% of net demand and time liabilities. Following a surge in reserve money and a decline in food credit in December 1987, the rate reached a significant 38% on January 2, 1988, to moderate excess liquidity.

- (i) In October 1993, incremental SLR for new liabilities was reduced from 30% to 25%.

- (ii) On October 14, 1995, a uniform valuation system for SLR securities was implemented.

- (iii) By April 13, 1996, NRE account SLR was rationalized from 30% to 25%.

Finally, on October 25, 1997, a uniform SLR of 25% was established for all scheduled commercial banks, aligning with the minimum requirements of Section 24 of the Banking Regulation Act, 1949. Today, the current SLR rate stands at 18%.

Important Historical Verification: Please note that older corporate finance listings or previous drafts specifying the modern SLR rate as 24% are outdated. Under modern RBI parameters, the ratio has been systematic lowered to 18% to expand commercial credit pathways.

Evaluate the Strategic Objectives and Macroeconomic Impact

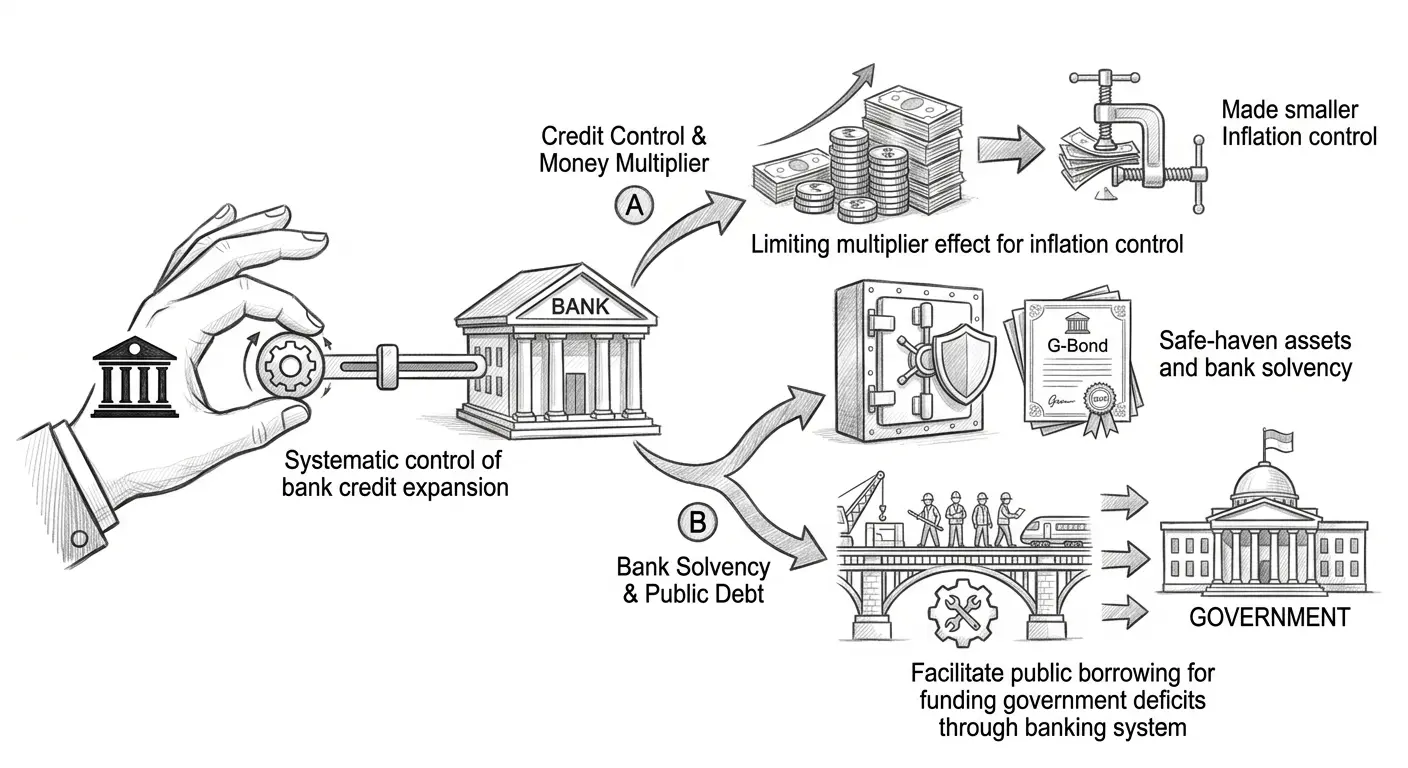

The overarching goal of the SLR policy is the systematic control of bank credit expansion. By modulating the required holdings of liquid assets, the RBI maintains a firm grip on credit creation.

Assessing Credit Control, Bank Solvency, and Public Debt

The primary impact of SLR is threefold. First, it acts as a tool for inflation control by limiting the money multiplier effect of banks. Second, it guarantees bank solvency by forcing institutions to hold safe-haven assets like government bonds. Third, it facilitates public borrowing, ensuring that the government can fund its deficits through the banking system at stable interest rates. During periods of high inflation, the RBI strategically raises the ratio to safeguard depositors' funds and curb excessive liquidity.

Summary

The Statutory Liquidity Ratio (SLR) remains a fundamental pillar of India's banking architecture. From its peak levels in the late 1980s to the streamlined 25% mandate established in 1997, the policy has successfully balanced the need for bank safety with the requirements of government fiscal policy. While it necessitates a reduction in commercial lending, the trade-off provides a stable environment for long-term economic growth and protects the financial integrity of the nation’s banking institutions against sudden liquidity shocks.

Quick Revision Points for Students

Reviewing the core empirical and regulatory facts ensures full retention for examinations.

- (i) The SLR is maintained by commercial banks within their own vaults in cash, gold, or approved securities, unlike the CRR which goes to the RBI.

- (ii) The ratio reached its historic peak of 38% in January 1988 to counter excess liquidity spikes.

- (iii) Financial reforms in October 1997 established a uniform floor rate of 25% under Section 24 of the Banking Regulation Act, 1949.

- (iv) In contemporary banking operations, the modern adjusted baseline rate stands at 18%.

Frequently Asked Questions (FAQ)

Q1: What are the eligible asset forms for fulfilling SLR mandates?

A1: Banks can park their funds in physical cash, valued holdings of gold, and government-approved unencumbered securities to fulfill statutory requirements.Q2: How did the SLR change during the peak stabilization era of 1987-1988?

A2: The ratio was adjusted upward from 37.5% in April 1987 to a record cap of 38% on January 2, 1988, driven by the need to balance an expanding reserve money profile.Q3: Where are SLR funds held compared to CRR reserves?

A3: SLR holdings are kept internally by the commercial banks themselves and can earn interest via coupon securities. Conversely, CRR holdings are cash deposits placed with the Reserve Bank of India that earn zero interest return yield metrics.