Future Development of Corporate Debt Market: Strategic Evolution and Policy Framework

Building a mature, highly liquid corporate bond market in India depends heavily on systemic transparency and reducing fragmented, off-market private deals. The transformation of this debt landscape aims to shift away from opaque bilateral agreements toward a standardized, exchange-driven ecosystem that matches the efficiency of the government securities market.

- Shifting to Public Pipeline

Regulators are placing a heavy emphasis on moving the market away from its traditional reliance on private placements and steering it toward a transparent public issue pipeline.

- Standardizing Infrastructure

The implementation of standardized clearing mechanisms is actively being pursued to safeguard investor interests across the board.

- Integrating Settlement Protocols

The integration of advanced settlement protocols is designed to cut down systemic risks and directly promote more vibrant secondary market trading.

Rationalising Primary Issuance and Clearing Mechanisms

To deepen the Indian financial system, regulatory bodies are focusing their energy on streamlining how bonds are born through primary issuance and how trades are finalized via central clearing.

Enhancing Primary Issuance and the Role of the Patil Committee

The story of market reform is incomplete without the Patil Committee, which served as the core architect for modernizing primary issuance procedures. The committee recognized that for the corporate debt market to flourish, it must reduce the overwhelming predominance of private placements, which naturally lack the transparency of public offerings.

- (i) Streamlining procedural requirements to make public debt issues far more attractive and less cumbersome for corporate issuers.

- (ii) Establishing a robust clearing mechanism specifically designed to mitigate settlement risks.

- (iii) Transitioning the market toward a centralized clearing and settlement environment to boost institutional investor confidence.

Evolution of Delivery versus Payment (DvP) Mechanisms

A critical pillar of market efficiency is the Delivery versus Payment (DvP) protocol, which ensures that the transfer of securities happens if and only if the corresponding payment is successfully made. The broad strategy involves a calculated migration from basic DvP I structures to the highly efficient DvP III standard.

Detailed Classification of DvP Types

The settlement framework relies on three distinct operational models:

DvP Type Settlement Mechanism Description Risk & Liquidity Impact DvP I Settles both funds and securities on a trade-by-trade basis. Minimizes counterparty settlement risk for individual contracts. DvP II Settles securities leg gross (contract-wise) but settles the funds leg on a net basis. Balances custom security transfers with aggregated cash cycles. DvP III Settles both funds and securities on a fully net basis at the end of the cycle. The gold standard of efficiency; allows for maximum liquidity optimization.

Tax and Regulatory Recommendations

Complex fiscal barriers have historically acted as a major deterrent for retail and institutional participation in corporate bonds, making targeted policy interventions absolutely necessary.

Strategic Fiscal Reforms: Stamp Duty and TDS Rationalisation

The Patil Committee pinpointed specific taxation hurdles that made corporate bonds less competitive than other instruments. By aligning the tax treatment of corporate debt directly with government securities, the goal is to establish a level playing field for all debt market participants.

- (a) Rationalisation of Stamp Duty: Harmonizing stamp-duty structures across different states removes geographical arbitrage and lowers the initial cost of issuance.

- (b) Abolition of TDS: Removing Tax Deduction at Source (TDS) for corporate bonds simplifies the investment lifecycle and drastically improves cash flow for bondholders.

Settlement Systems and Foreign Investment Dynamics

As the core clearing infrastructure matures, policy focus shifts naturally toward integrating foreign portfolio investment and expanding market repo capabilities.

Market Repos and International Capital Management

The RBI has laid out a clear roadmap where market repos in corporate bonds will be fully permitted once DvP III and STP (Straight Through Processing) standards are universally adopted. This operational shift will allow corporate debt to be utilized as high-quality collateral, which will significantly increase secondary market liquidity.

- (i) Using medium-term management of foreign investment limits in both government securities and corporate debt as an active tool for capital account management.

- (ii) Transitioning toward a much more liberalized regime for foreign investors once the domestic debt ecosystem hits safety and depth milestones.

Pre-requisites for a Liberalised Investment Regime

For the corporate bond market to open safely to global capital pipelines, the RBI and SEBI require three fundamental milestones to protect economic stability.

- (i) Ensuring a fully operational, safe, and highly efficient settlement infrastructure is active across exchanges.

- (ii) Achieving a consolidated public debt-to-GDP ratio of below 50 per cent to ensure long-term fiscal sustainability.

- (iii) Developing sufficient market depth through the mandatory and active participation of large insurance and pension funds.

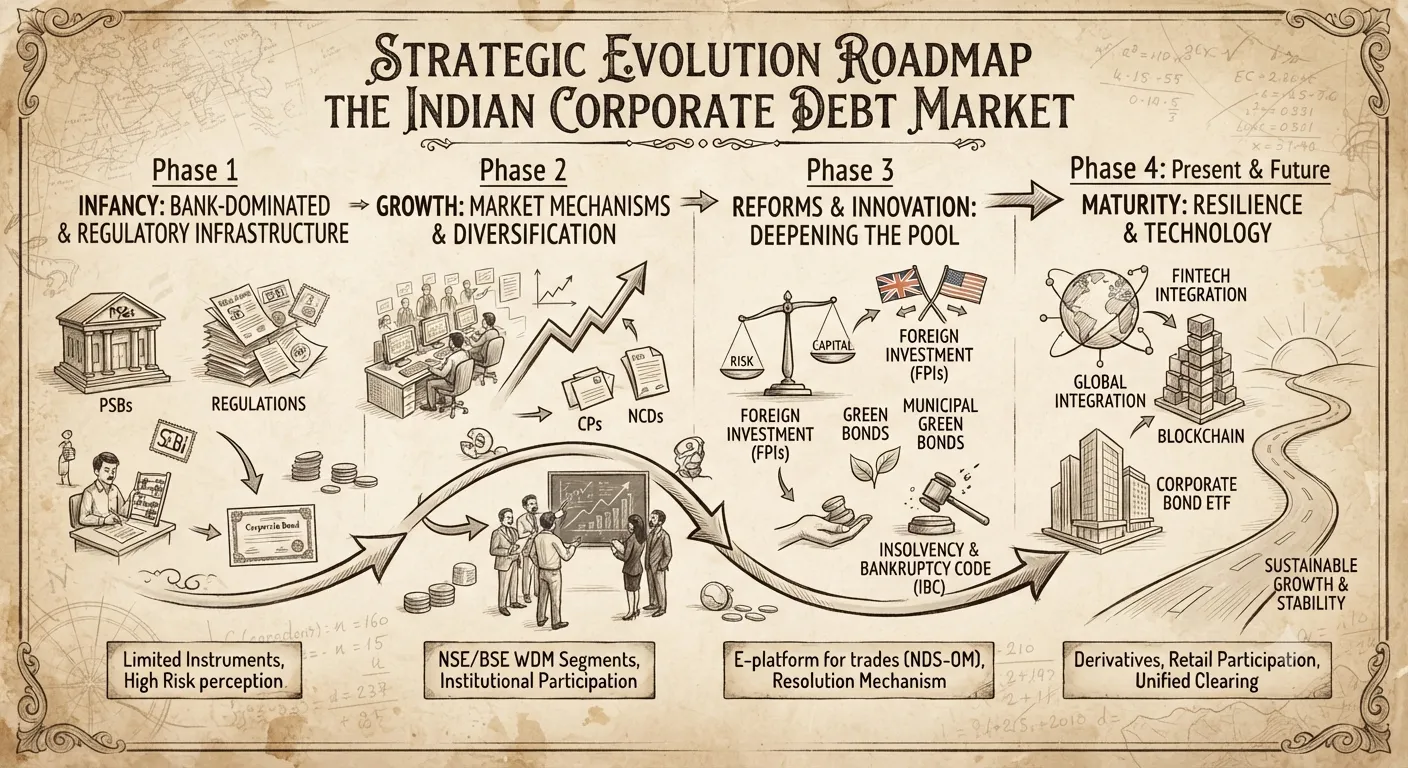

Structural Foundations and Policy Framework

Looking closely at the historical dominance of G-Secs provides the necessary context for why the corporate side of the market is only now emerging as a major financial powerhouse.

From Fiscal Dominance to a Vibrant Corporate Ecosystem

Historically, Government securities completely dominated the debt market because of deep fiscal dominance and a noticeable lack of contractual savings options. During that era, banks acted as the sole primary investors, often engaging in closed private placements rather than transparent trading. However, the ecosystem is shifting rapidly with the expansion of mutual funds and the insurance sector.

- (i) The rise of contractual savings institutions now provides the steady, long-term capital pool required for corporate debt absorptions.

- (ii) The implementation of Robust systems for reporting and trading ensures accurate, real-time price discovery.

- (iii) The ongoing execution of Patil Committee recommendations by relevant agencies is finalizing the modern policy framework.

Summary and Strategic Review

Understanding the historical transition from administered interest rates to a market-driven economy is crucial for students of economics and finance. While the G-Sec market has matured significantly since 1991 through auction-based discovery and institutional mechanisms like LAF and MSS, the corporate bond market has faced persistent challenges of low liquidity and structural barriers, despite reforms initiated after the 2007 SEBI reforms. The systematic implementation of Patil Committee recommendations, the adoption of DvP III, the rationalisation of stamp duty, and SEBI’s streamlining efforts have collectively strengthened settlement efficiency and market depth, contributing to the economic stability of India. These reforms are central to understanding the modern Indian financial system, its regulatory framework, and the evolving capital market. For students, mastering these concepts—from cost of capital and fiscal ratios to macroeconomic stability and the future investment climate—is essential for analysing India’s long-term financial sector reforms.

Quick Revision Points for Students

Reviewing the core empirical and geographical facts ensures full retention for examinations.

- (i) Market Shift: Moving away from fragmented, opaque bilateral private placements toward transparent, exchange-driven public issues.

- (ii) Settlement Standard: Transitioning from DvP I to DvP III, which enables net settlement of both funds and securities to optimize liquidity.

- (iii) Fiscal Alignment: The Patil Committee recommended harmonizing stamp duty across states and abolishing TDS to create a level playing field with G-Secs.

- (iv) Global Capital Pre-requisites: Opening the debt market fully to international portfolios requires a consolidated public debt-to-GDP ratio below 50 per cent and active participation from pension and insurance funds.

Frequently Asked Questions (FAQ)

Q1: What did the Patil Committee identify as the primary challenge in India's corporate debt market?

A1: The committee highlighted an overwhelming pre-dominance of private placements, which lack the market transparency and secondary market liquidity of structured public offerings.Q2: What is the main operational advantage of migrating to a DvP III settlement framework?

A2: Unlike DvP I, which settles trades individually, DvP III nets both the funds leg and the securities leg, which drastically lowers counterparty risk while ensuring maximum liquidity optimization.Q3: What macro-fiscal condition must be met before fully liberalizing foreign investments in Indian corporate bonds?

A3: The Reserve Bank of India and SEBI require the country's consolidated public debt-to-GDP ratio to fall below 50 per cent to ensure overall fiscal sustainability and macroeconomic stability.