The Repurchase Agreement (Repo) and Banker’s Acceptance serve as the foundational pillars of the modern money market, providing essential short-term liquidity and credit security. While Repo transactions act as the primary steering wheel for the Reserve Bank of India (RBI) to control the money supply, Banker’s Acceptances function as critical trade-finance instruments that bridge the trust gap between global buyers and sellers. Understanding these tools is vital for grasping how interest rate corridors are maintained and how corporate debt is liquidated effectively in the secondary market.

Mastering Repurchase Agreements (Repo and Reverse Repo)

In the high-stakes environment of overnight borrowing, Repurchase transactions—commonly known as Repo or Reverse Repo—provide a secure framework where two parties agree to sell and subsequently repurchase the same security. These arrangements are strictly regulated and restricted to entities and assets approved by the Reserve Bank of India (RBI). To ensure safety, eligible securities are limited to high-quality assets including Government of India (GOI) securities, State Government securities, Treasury Bills (T-Bills), PSU Bonds, and Financial Institution (FI) Bonds, as well as Corporate Bonds.

- The Strategic Nature of Collateralized Borrowing

The foundational bedrock of a repo deal rests entirely upon its underlying collateral asset structure. By anchoring the credit swap to top-tier government and sovereign backed papers, systemic defaults are virtually eliminated, transforming the process into an incredibly safe short-term haven for deploying institutional cash reserves dynamically.

The Core Nature and Eligible Securities of Repo Deals

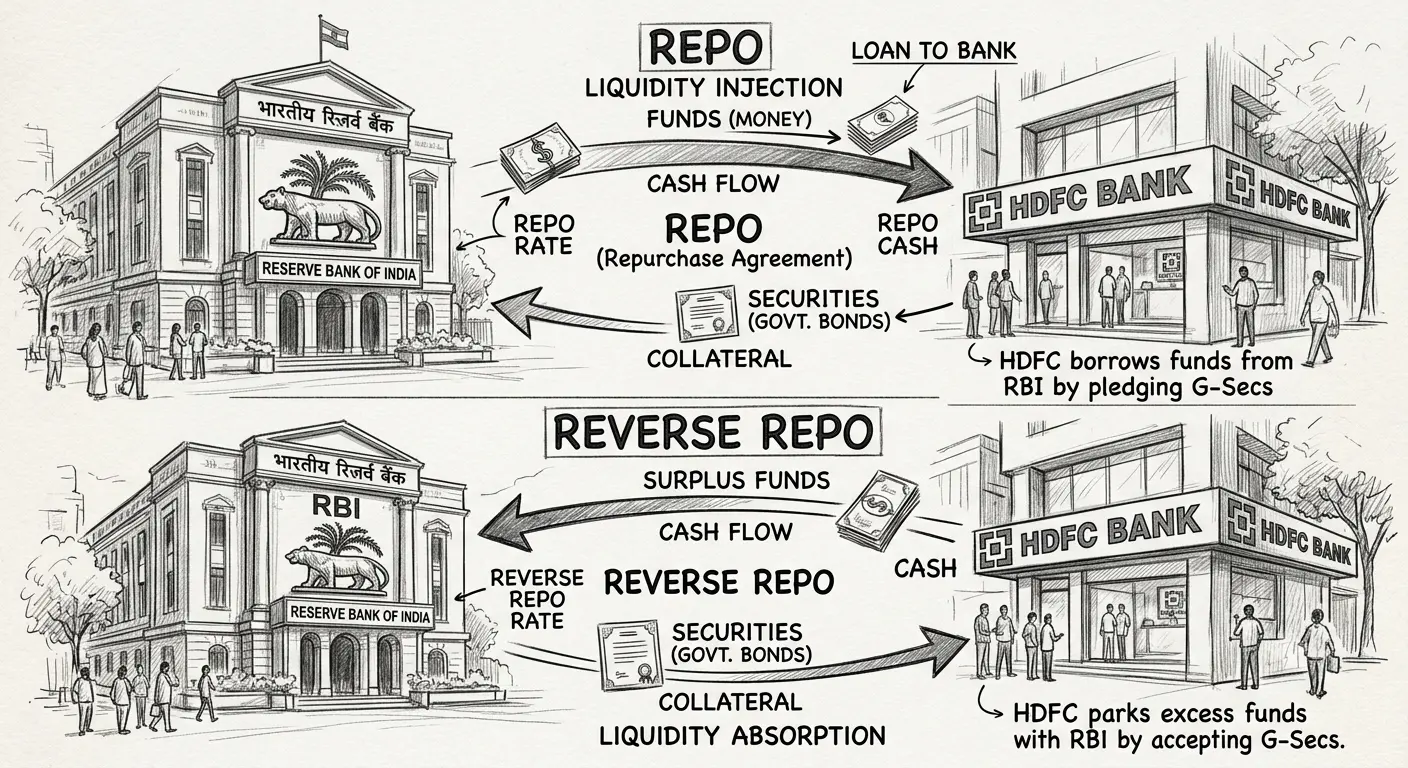

The beauty of a Repo agreement lies in its dual perspective. For the seller, it is a commitment to sell a security today with a firm promise to buy it back at a predetermined price and date. From the buyer's vantage point, this exact same transaction is a Reverse Repo, where they agree to purchase the asset now and sell it back later. This relationship defines the Repo Rate: the interest rate that represents the compensation paid by the borrower (the seller) to the lender (the buyer) for the duration of the agreement.

Mechanism: How Sellers and Buyers Navigate Repo Rates

Understanding the flow of these transactions is key to identifying market liquidity trends. When a bank needs immediate cash, it enters a Repo; when it has excess funds, it seeks a Reverse Repo to earn interest safely.

- (i) The Repo perspective belongs to the party seeking short-term liquidity, utilizing assets to draw operational capital instantly.

- (ii) The Reverse Repo perspective belongs to the party providing the funds, positioning cash to harvest safe returns over fixed horizons.

The Strategic Role of RBI in Managing Economic Liquidity

The RBI utilizes these mechanisms as surgical tools for monetary policy. By adjusting these rates, the central bank influences the entire interest rate corridor. Currently, the Repo rate stands at 5.50%, serving as the floor rate for the money market, while the Reverse Repo rate is positioned at 3.35% (as of 06 Jun 2025). These rates work in tandem with the bank rate to keep market volatility within a controlled ceiling and floor.

Liquidity Injection and Absorption Strategies

The RBI intervenes based on the inflationary or deflationary needs of the economy through specific transactional directions.

- (i) To absorb liquidity and curb inflation, the RBI raises borrowing metrics or enters into strategic Repo transactions to lock away float capital.

- (ii) To inject liquidity and stimulate growth, the RBI utilizes Reverse Repo operations, shifting accessible money directly back to retail banking loops.

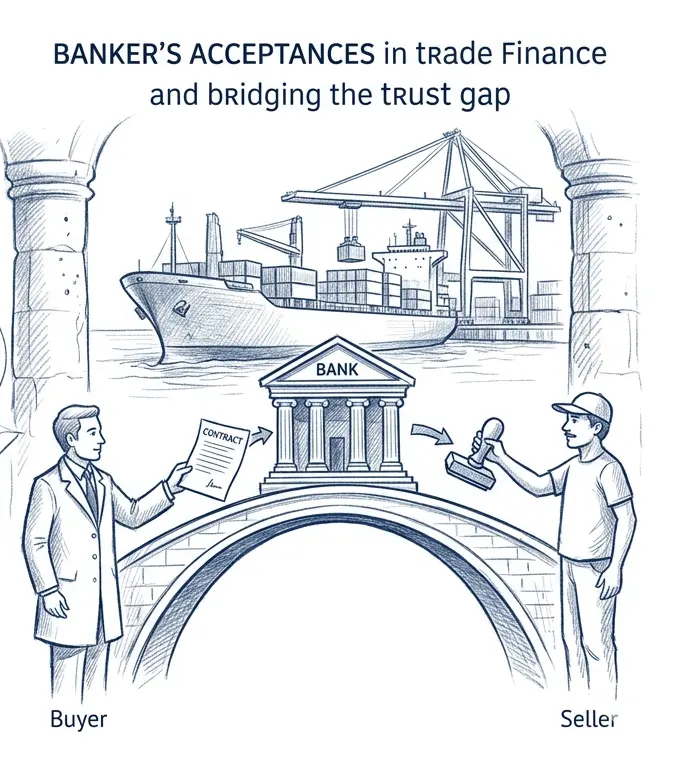

The Mechanics of Banker’s Acceptance in Trade Finance

A Banker’s Acceptance is a specialized short-term credit investment that facilitates commerce by substituting a bank's creditworthiness for that of a private firm. It originates as a bill of exchange drawn by a corporation, which is then guaranteed (accepted) by a bank. This guarantee ensures that a specified payment will be made on a fixed future date, backed by a claim on the underlying goods acting as collateral.

- The Structural Blueprint of Cross-Border Trade Assurances

When businesses navigate complex international import and export channels, basic corporate promises are rarely enough to satisfy sellers across distant shores. The banker's acceptance steps into this vacuum by elevating a private commercial invoice into an unassailable bank-certified asset that institutions treat with absolute trust.

Structure and Guarantee Framework of Banker’s Acceptance

For these instruments to remain tradable in the secondary market, the drawer must maintain a superior credit rating. Corporations leverage these as negotiable time drafts to finance the complexities of imports and exports, particularly when the creditworthiness of an international trading partner is unverified.

Creditworthiness and Tradability in Secondary Markets

The structural life cycle and dynamic flexibility of these acceptances are governed by precise, trade-friendly terms:

- (i) Standard maturity terms usually hover around 90 days, matching standard global logistics timelines.

- (ii) Flexible durations can range from 30 to 180 days based on unique shipping or seasonal industry trade needs.

Maturity Cycles and Liquidating Receivables Early

One of the primary advantages for the seller is that they are not required to hold the Banker's Acceptance until the end of its term. If immediate cash is needed, the holder can liquidate receivables by selling the instrument in the secondary market at a discount from its face value. This high level of tradability makes it a preferred choice for corporations managing global supply chains.

Money Market Summary Revision Capsule

Reviewing core money market characteristics establishes operational readiness for professional evaluation:

- (i) Repos are collateralized short-term borrowing mechanisms anchored firmly to sovereign and government papers.

- (ii) The RBI Policy Corridor leverages a 5.50% Repo Rate and 3.35% Reverse Repo Rate to balance domestic money supply.

- (iii) Banker's Acceptances turn raw corporate bills into highly liquid time drafts backed by an accepting bank's seal.

- (iv) Holders can seamlessly liquidate receivables early by dealing acceptances at secondary market discounts.

Frequently Asked Questions (FAQ)

Q1: What marks the main difference between a Repo and an unsecured money market loan?

A1: A Repo transaction is fully collateralized by top-tier assets such as GOI Securities or T-Bills, ensuring structural safety, whereas unsecured loans depend entirely on the borrower's standalone promise to repay.Q2: How does a Banker's Acceptance insulate global exporters from cross-border payment risks?

A2: By substituting the financial creditworthiness of an accepting bank in place of an unknown foreign buyer, the exporter is assured of payment on the due date regardless of the importer's personal liquidity condition.Q3: Can a corporation sell a Banker's Acceptance before its official maturity date?

A3: Yes, corporations can easily liquidate receivables early by trading the instrument in active secondary money markets at a calculated discount rate beneath its original face value.Summary

In conclusion, Repo and Reverse Repo transactions act as the pulse of national liquidity, dictated by the RBI's strategic rates to maintain an interest rate corridor. Simultaneously, Banker’s Acceptances provide the financial bridge for global trade, turning unsecured bills into bank-guaranteed negotiable drafts. Together, these instruments ensure that whether for a central bank managing the money supply or a corporation financing an export, the short-term money market remains efficient, liquid, and secure for all participants.