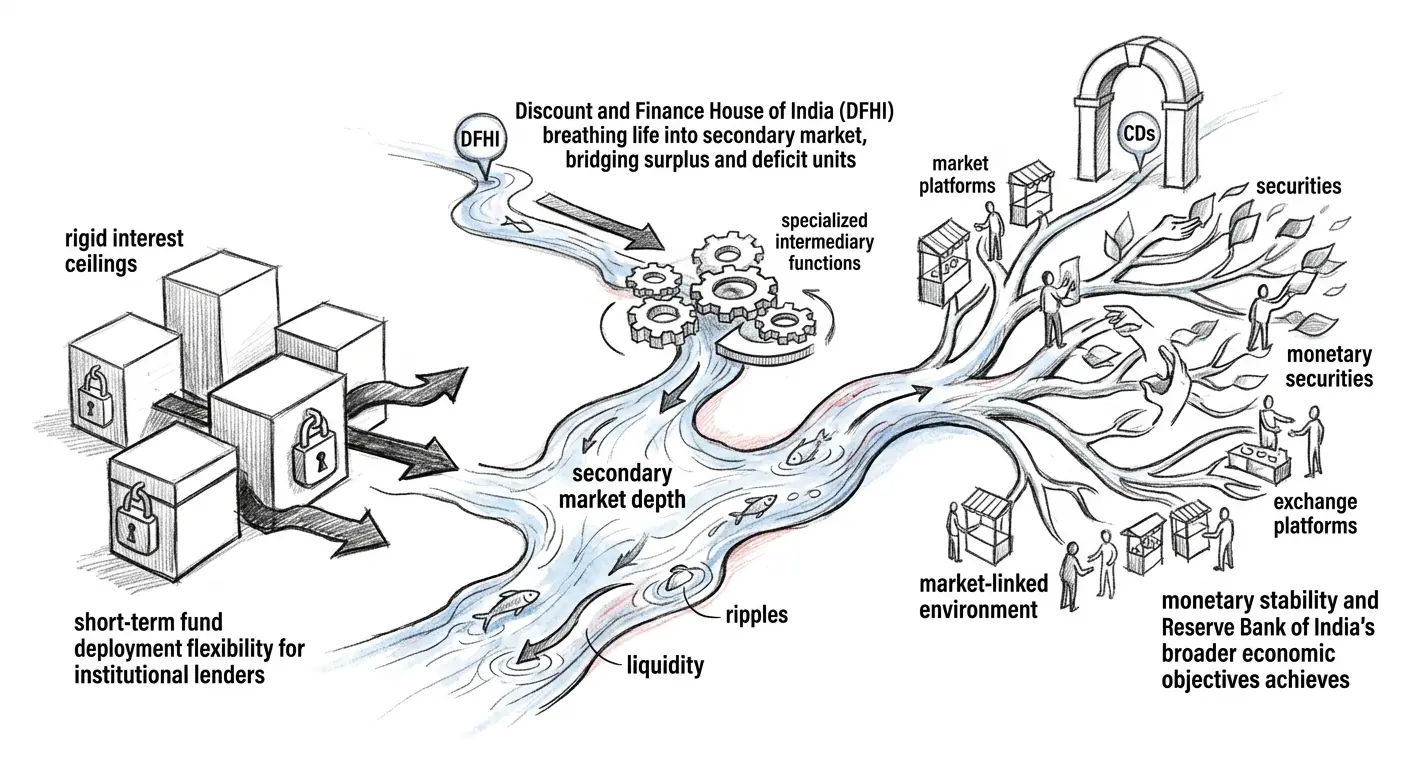

The Discount and Finance House of India (DFHI) and Certificate of Deposits (CDs) serve as the fundamental architecture for maintaining liquidity and secondary market depth within the Indian financial system. Established during the late 1980s, these entities and instruments transitioned the economy from rigid interest ceilings to a market-linked environment. The significance of this evolution lies in its ability to provide short-term fund deployment flexibility for institutional lenders and monetary stability for the Reserve Bank of India's broader economic objectives.

Institutional Framework for Money Market Stability

- The Narrative Genesis of Secondary Market Liquidity

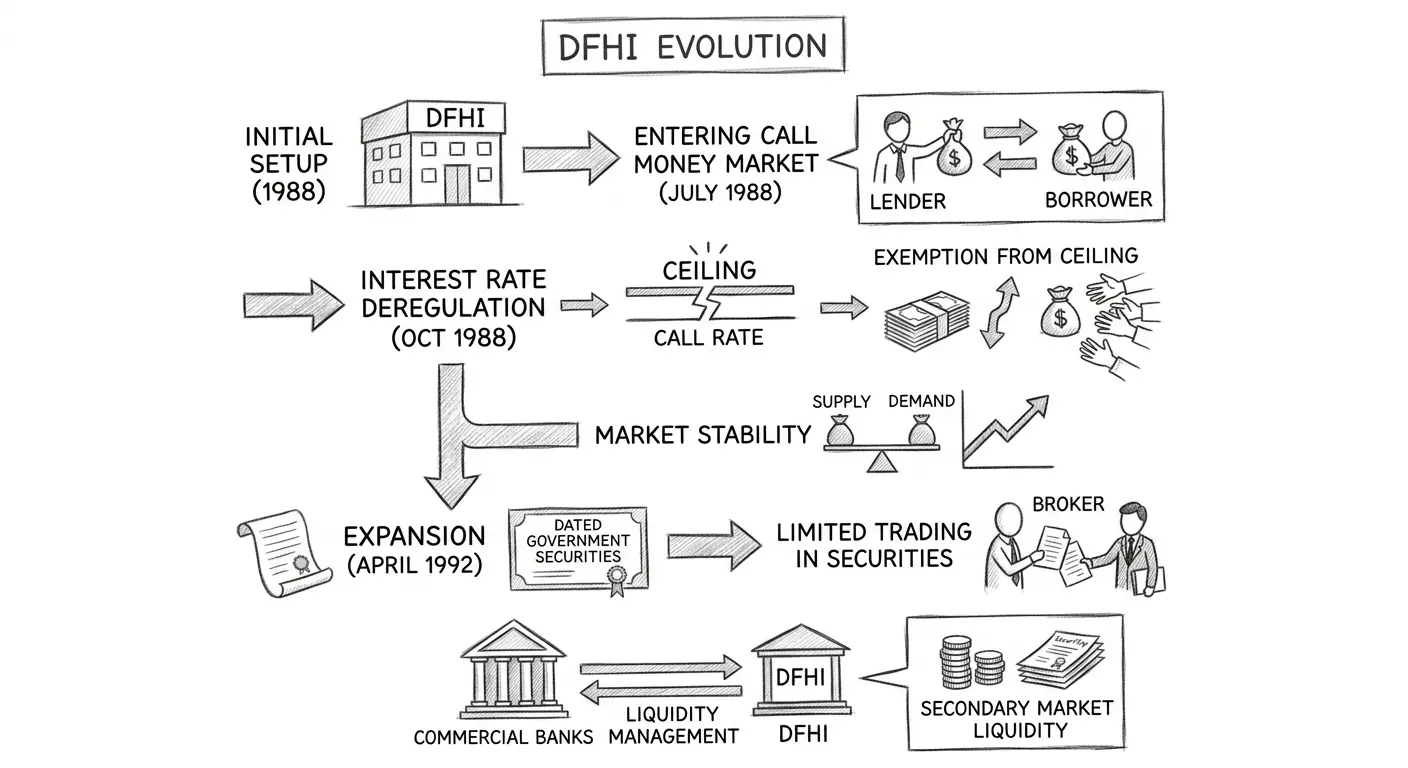

The creation of the Discount and Finance House of India (DFHI) marked a pivotal moment in Indian financial history. Its primary mission was to breathe life into the secondary market for money market instruments, ensuring that assets could be traded efficiently rather than held until maturity. By acting as a specialized intermediary, DFHI bridged the gap between surplus and deficit units in the economy, providing a sophisticated platform for the call and notice money markets.

In-Depth Analysis of the Discount and Finance House of India (DFHI)

The DFHI began its journey to transform the inter-bank lending landscape through strategic interventions and policy exemptions that favored market-driven discovery.

Analyze the Market Operations and Deregulation Milestones

On July 28, 1988, the DFHI was formally permitted to enter the call and notice money markets, functioning as both a lender and a borrower. To ensure the institution had the necessary agility, the Indian Banks’ Association granted a critical exemption from the interest rate ceiling in October 1988. This move was a cornerstone of partial deregulation, allowing call money rates to fluctuate based on actual demand and supply, thereby enhancing money market stability. By April 2, 1992, the scope of DFHI expanded into limited trading of dated government securities, further maturing the secondary market.

- (i) Participation in Call Money Markets enabled better liquidity management for commercial banks.

- (ii) Trading in Dated Securities provided a foundation for long-term government debt liquidity.

Understanding Certificate of Deposits (CDs) as Investment Vehicles

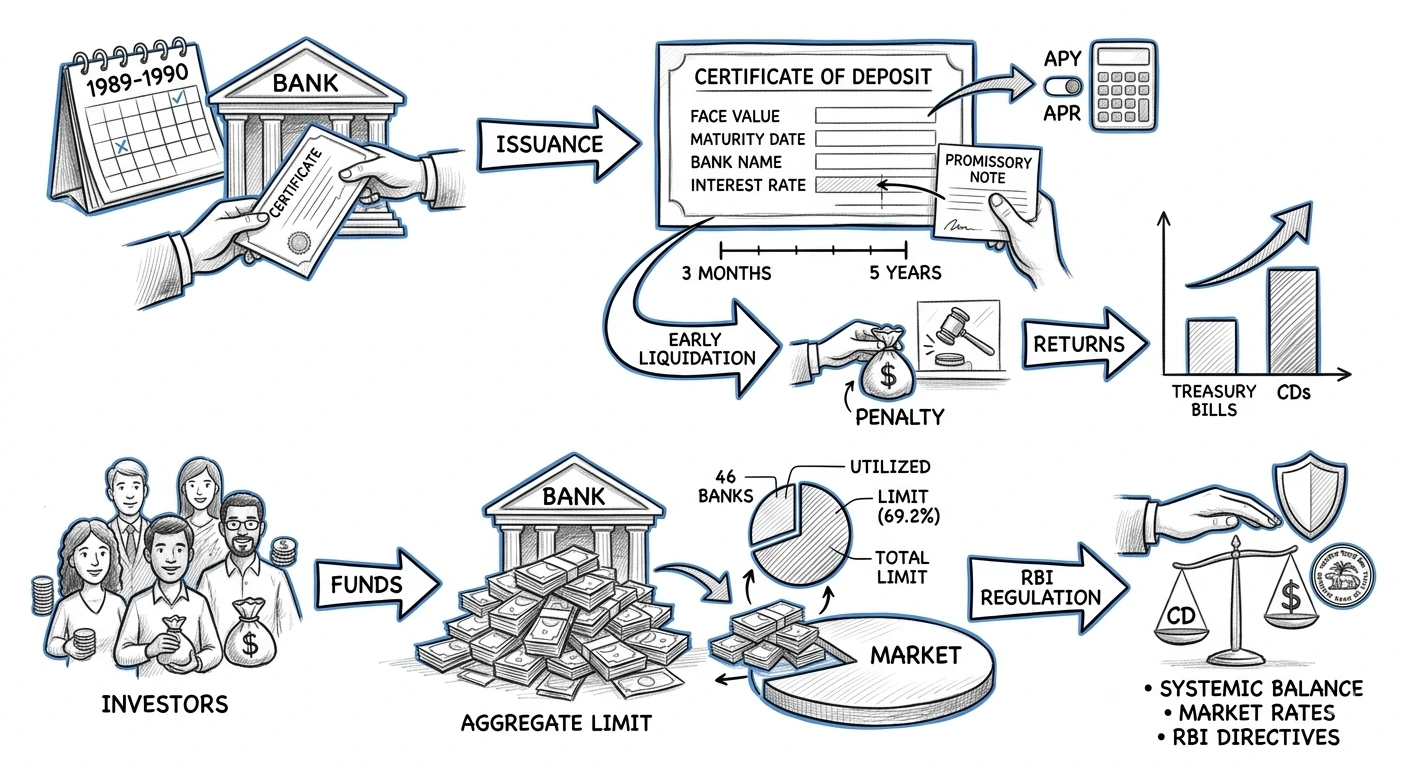

Introduced during the first half of 1989–90, Certificate of Deposits (CDs) emerged as a negotiable alternative to traditional term deposits, offering institutions a way to raise short-term resources competitively.

Evaluate the Technical Characteristics and Yield Calculations of CDs

A CD functions as a short-term borrowing note, similar to a promissory note, issued in certificate form with a fixed face value and maturity date. Typically maturing between 3 months to 5 years, these instruments are non-withdrawable on demand; however, they can be liquidated early subject to a penalty. The returns on CDs are notably higher than Treasury Bills, reflecting the slightly higher risk profile of the issuing scheduled commercial banks or financial institutions.

The yield logic is divided into two primary metrics: Annual Percentage Rate (APR), which utilizes simple interest, and Annual Percentage Yield (APY). While both are identical if interest is paid annually, APY becomes significantly more beneficial when interest is compounded more than once a year.

Summary

By February 22, 1991, the CD market showed immense scale, with 46 major scheduled commercial banks issuing ₹3,035 crore, utilizing 69.2% of their ₹4,383 crore limit. The regime shifted towards full market-determined interest rates in 1992–93, allowing banks to raise funds based on their creditworthiness. To maintain systemic balance, the RBI capped CD issuance at 10% of average outstanding deposits as of April 17, 1993. Further accessibility was achieved on April 15, 1997, when the minimum investment size was lowered from ₹25 lakh to ₹10 lakh. Today, CDs remain vital negotiable instruments, governed by RBI directives and issued as either dematerialised units or Usance Promissory Notes.

Quick Revision Points for Students

Reviewing the core operational milestones ensures full readiness for competitive examinations.

- (i) The DFHI was established in the late 1980s to stimulate the secondary money market and build operational velocity for liquidity.

- (ii) In October 1988, the Indian Banks' Association exempted DFHI from interest ceilings, paving the path for market-driven inter-bank operations.

- (iii) Certificate of Deposits (CDs) were introduced in 1989-90 as transferable, negotiable short-term instruments.

- (iv) Regulatory changes on April 15, 1997, dramatically improved retail access by dropping the minimum investment ticket size from ₹25 lakh to ₹10 lakh.

Frequently Asked Questions (FAQ)

Q1: When did DFHI gain approval to operate directly inside call and notice money markets?

A1: The DFHI officially entered these specific markets on July 28, 1988, taking up positions as both a formal borrower and lender.Q2: What happens if an investor decides to cash out a Certificate of Deposit ahead of schedule?

A2: CDs are legally designed to be non-withdrawable on demand, meaning early liquidations trigger an immediate financial penalty imposed by the issuing institution.Q3: What distinguishes the calculation baseline between CD interest parameters?

A3: APR relies strictly on a standard simple interest model, whereas APY factoring tracks structural earnings growth when interest compounding triggers multiple times across a calendar year.