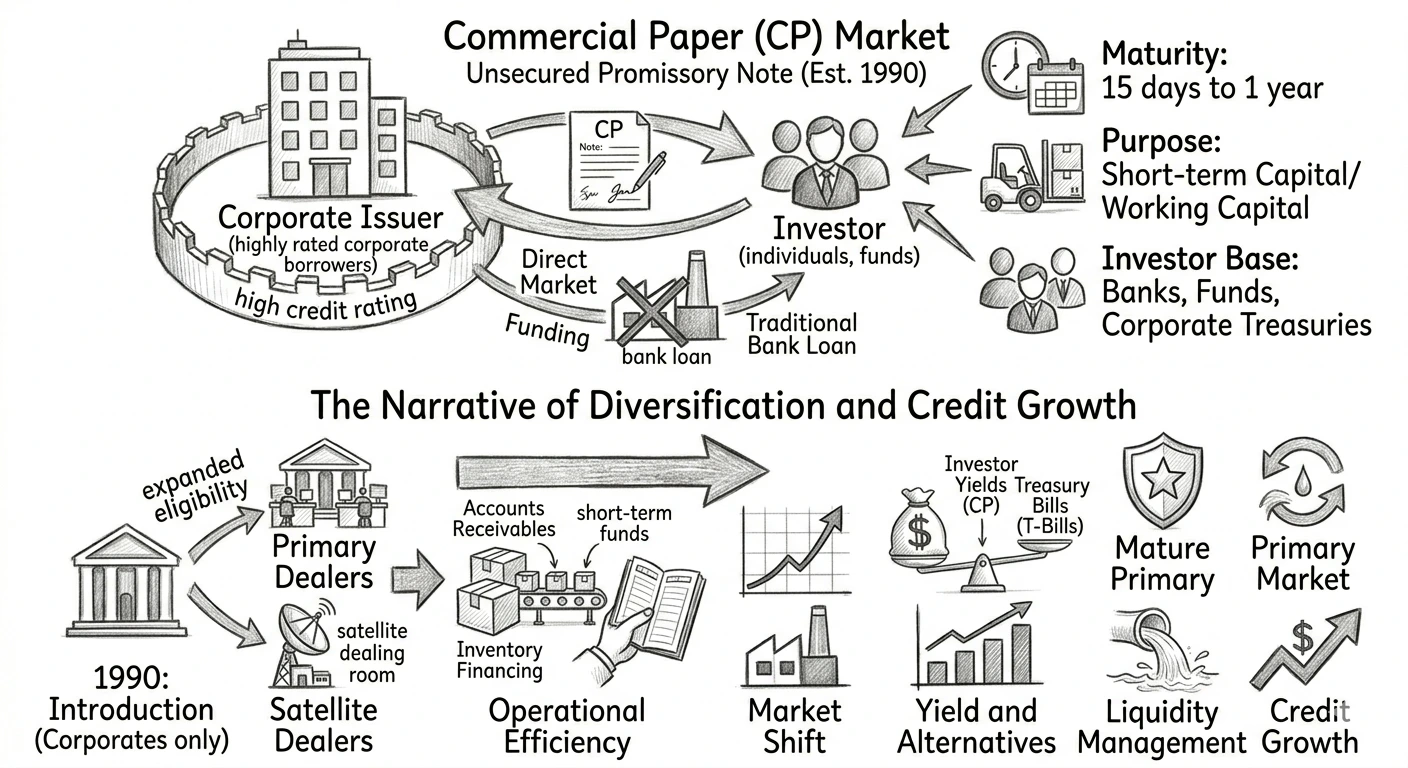

The Commercial Paper (CP) market acts as a vital cog in India's overall financial machinery. Operating as an unsecured money market instrument issued in the form of a promissory note, it provides a crucial bridge for high-end corporate liquidity. Originally launched in 1990, its main significance lies in allowing highly rated corporate borrowers to diversify their resource mobilization mixes and secure short-term capital directly from institutional investors. By structuring a reliable alternative to standard bank credit, CPs have fundamentally transformed the liquidity landscape, helping elite firms manage operational demands smoothly while offering investors short-term returns that typically beat standard Treasury Bills.

Commercial Paper (CP) in India: Features, Evolution, and Regulatory Changes

The roll-out of Commercial Paper triggered a major shift toward structural diversification within India's primary money market. The deployment framework ensures high-grade institutions gain quick financial access while preserving investor security through rigid baseline benchmarks.

- The Narrative of Diversification and Credit Growth

While the instrument was originally tailored exclusively for stable corporate houses, eligibility rules were later opened up to cover both primary dealers and satellite dealers. This change allowed core market intermediaries to successfully address their intense, short-term funding needs for daily operations. Featuring fixed maturity periods running between 15 days to 1 year, CPs established themselves as the premier option for funding accounts receivables and settling immediate inventory financing issues without experiencing the bureaucratic processing delays typical of traditional bank loans.

Definition and Strategic Purpose of Commercial Paper

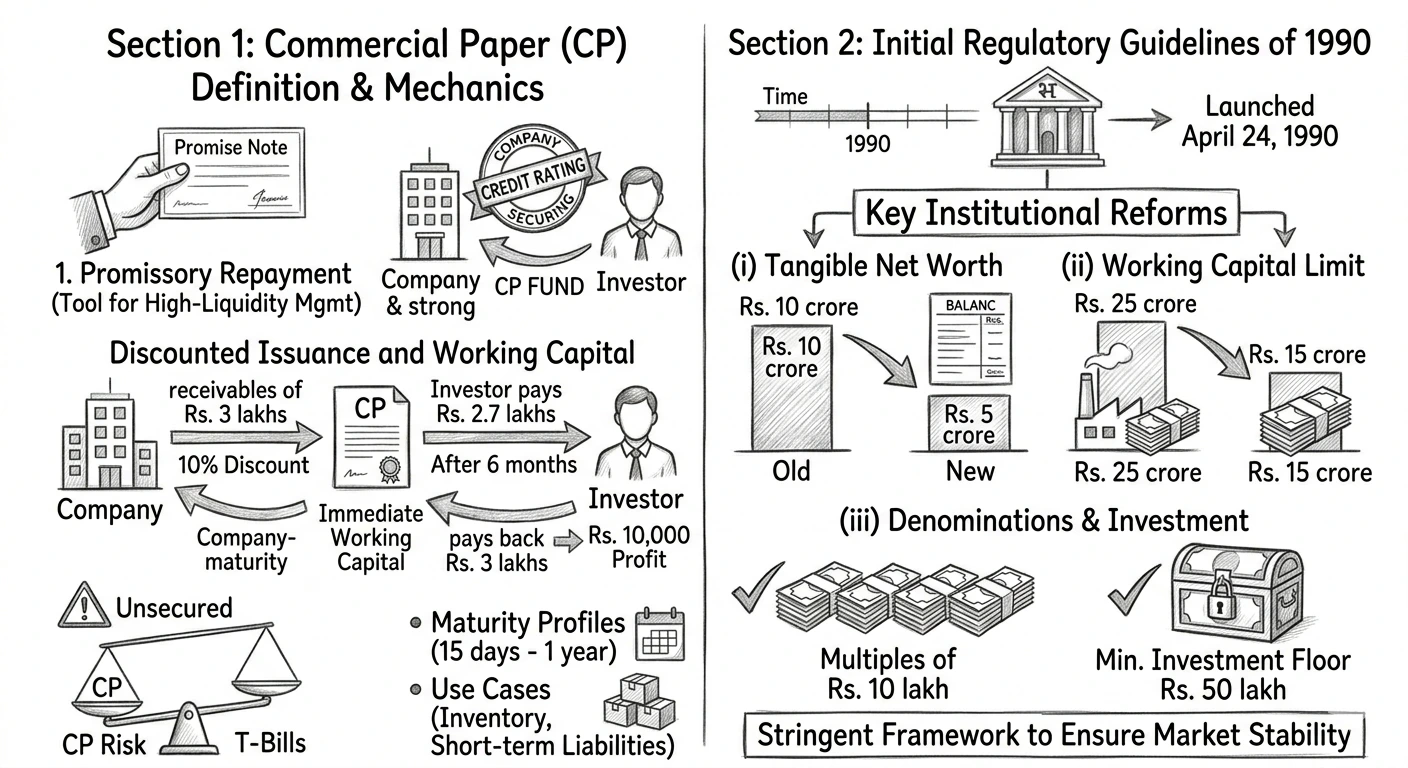

Stripped to its fundamentals, a CP functions as a legally binding promise of short-term repayment. It acts as a specialized tool for high-liquidity management, where corporate entities translate their strong credit reputation into immediate cash by offering notes at a discount.

Operational Mechanics and Liquidity Benefits

The underlying mechanics of a CP revolve entirely around its discounted issuance system. For example, a business holding Rs. 3 lakhs in book debts due in 6 months can choose to float a CP at an upfront 10% discount. This step instantly unlocks necessary working capital for the firm, while the buying investor pockets a clear Rs. 10,000 profit when the note matures at full face value. However, because these obligations remain completely unsecured, only companies carrying the highest credit ratings can successfully attract market investors without paying out unsustainably steep discount rates, balancing their risk position relative to safer T-Bills.

- (i) Maturity profiles run flexibly inside a 15-day to 1-year boundary.

- (ii) Primary use cases focus on managing inventories and clearing temporary liabilities.

Analyzing the Initial Regulatory Guidelines of 1990

Brought into active force on April 24, 1990, the foundational setup for issuing CPs carried highly stringent entry barriers. These defensive institutional guidelines were specifically implemented by the central bank to avoid defaults and systematically build up long-term secondary market depth.

- Conservative Operational Safeguards

The early setup targeted only premium market players, ensuring that the new money market tool remained stable during its initial adoption phase across the financial ecosystem.

Key Institutional Reforms Introduced in April 1990

The Reserve Bank of India laid down rigid minimum operational baselines to preserve market health right from its initial launch:

- (i) The corporate tangible net worth requirement was placed at a minimum of Rs. 5 crore.

- (ii) The fund-based working capital limit of the company had to stand at Rs. 15 crore or more.

- (iii) The total CP issue size was strictly capped at a maximum of 20% of the firm's overall working capital limit.

- (iv) Denominations were standardized in multiples of Rs. 10 lakh, backed by a minimum single-investor floor of Rs. 50 lakh.

- (v) Maturity timelines were restricted within a tighter 3 to 6 months operational window.

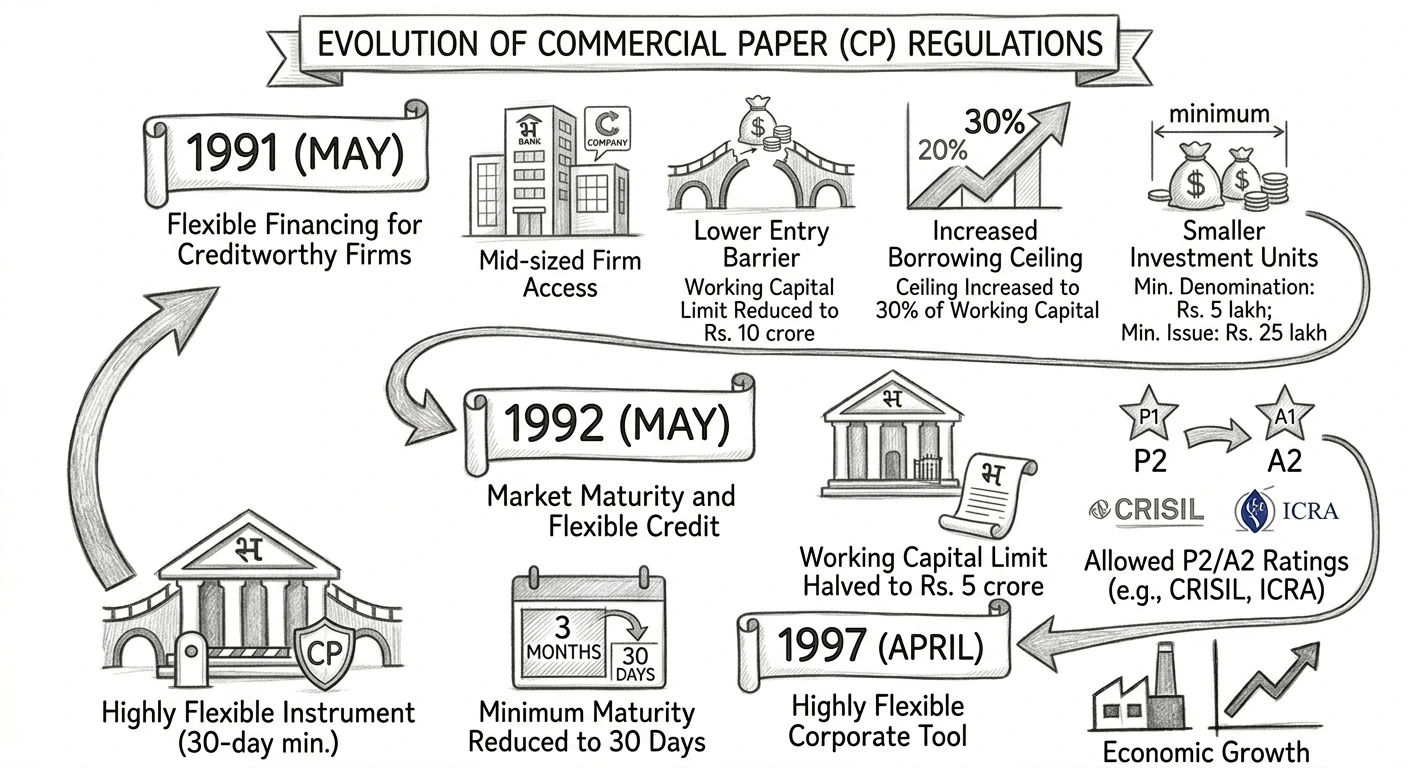

Evaluate Further Regulatory Reforms in 1991

By May 30, 1991, rising corporate demands for highly responsive short-term financing forced the implementation of a second wave of reforms. These strategic adjustments focused on easing entry barriers for well-managed, mid-sized corporate entities.

- Broadening Market Access and Issuance Volume

The policy revisions altered structural limits to let smaller, creditworthy companies participate, which enhanced overall asset availability in the short-term credit market.

Detailed Breakdown of May 1991 Policy Adjustments

The 1991 regulatory upgrades adjusted the core borrowing ceiling and scaled down purchase minimums to attract a wider group of retail and institutional buyers:

- (i) The entry floor for fund-based working capital was slashed down to Rs. 10 crore.

- (ii) The maximum issuance cap was raised from 20% to 30% of the company's working capital limit.

- (iii) Minimum paper denominations were lowered to Rs. 5 lakh, while the minimum entry investment per investor was cut in half to Rs. 25 lakh.

Evolutionary Updates and Relaxations in 1992 and 1997

The systematic maturation of the Commercial Paper space hit its stride through progressive policy updates across the late 1990s. These changes shifted CPs from a rigid niche option into a highly adaptable corporate tool.

- Credit Deregulation and Structural Integration

By dropping entry floors and opening up acceptable rating brackets, regulators successfully converted the CP market into a primary pillar of corporate liquidity management.

Criteria for Credit Rating and Maturity Flexibility

On May 2, 1992, the mandatory working capital limit threshold dropped to just Rs. 5 crore. This round of adjustments also saw a meaningful relaxation of credit ratings; instead of forcing a strict P1/A1 rating requirement, firms holding P2/A2 grades (issued by agencies like CRISIL and IICRA) were cleared to raise funds. Ultimately, the landmark update on April 15, 1997, which cut the minimum maturity down from 3 months directly to 15 days, solidified the CP's role as a highly flexible and ultra-responsive market instrument.

Summary: The Maturation of the Indian Money Market

The structural development of the Commercial Paper market reflects India’s ongoing transition toward a highly flexible, non-bank financial landscape. By moving from the tight caps of 1990 to highly accessible credit frameworks and ultra-short 15-day maturities, CPs have grown into an invaluable asset class for balancing immediate corporate cash demands with institutional investor needs.

Quick Revision Points for Students

Reviewing these core historical benchmarks ensures accurate retention for examinations:

- (i) CPs are unsecured promissory notes issued at a discount, serving as key short-term money market tools.

- (ii) The initial 1990 baseline required a Rs. 5 Cr net worth and a Rs. 15 Cr working capital limit, with issuance capped at 20%.

- (iii) The 1991 revisions lowered the working capital floor to Rs. 10 Cr and bumped the maximum issuance ceiling up to 30%.

- (iv) The 1992 reforms opened the market to P2/A2 credit ratings and dropped the working capital entry floor to Rs. 5 Cr.

- (v) The April 1997 deregulation dramatically slashed the minimum maturity period down to 15 days.

Frequently Asked Questions (FAQ)

Q1: What exactly makes Commercial Paper an unsecured money market instrument?

A1: CPs are backed completely by the general credit reputation of the issuing corporation instead of being tied to specific physical collateral, meaning investors take on a slightly higher credit risk compared to secured assets or T-Bills.Q2: How did the 1991 policy adjustments help mid-sized businesses in India?

A2: The 1991 reforms slashed the required working capital entry floor to Rs. 10 crore, lifted the borrowing limit to 30%, and cut the minimum individual investment size to Rs. 25 lakh, making it easier for smaller firms to issue paper.Q3: What major maturity change occurred in April 1997?

A3: On April 15, 1997, the regulatory authority reduced the minimum maturity period of CPs from 3 months down to 15 days, providing elite firms with unmatched short-term liquidity management options.